“The graveyards are full of indispensable men!” — attributed to Napoleon Bonaparte

In his eponymous autobiography, Michael Bloomberg wrote:

I want the loss of anyone in the company to hurt us, but not fatally, including the likes of me. Every job performance review I give my direct-reporting managers includes the question, ‘Who’s your replacement? If you don’t have one now, I can’t consider you for bigger things. If you don’t have one the next time I ask, you may no longer be a direct report.

One of the most important jobs of a great leader is to attract great talent. How adaptable you are as a firm depends in part upon how your company is organized, but most of all it depends upon the people operating it. Internal leaders are sometimes secretly afraid to bring in ultra-talented employees because they fear that these newcomers could challenge their status at the firm. A talented executive whose interests are aligned with the firm’s and is confident in her role will always recruit stars who exceed herself in various ways, but one who is worried about her value to the firm will not.

A great leader should make it clear to her team members that as a matter of culture her job is to replace herself. A new hire should know from the outset that she will ultimately have to bring in new talent to replace herself so that she can personally better herself and achieve loftier goals. A policy of knowing your replacement is one of the best ways to drive a growth culture. It anticipates and eliminates the most harmful politics in leadership for an expanding company, and instantly sets the right tone for a high talent, growth mindset executive team.

Moreover, to craft a truly durable company you have to plan for as many contingencies as possible. Many contingencies are all-too-human variables: injuries, illnesses, changes-of-plans, early retirements and so on. Vacancies in your company’s structure are essentially unpredictable, and can be very costly. The departure of key individuals kills morale, loyalty and productivity among your employees. Great leaders are paranoid by nature and always plan for contingencies. They always ask: “Where are the bottlenecks? Which people can I not afford to lose?”

Questions of management depth extend beyond hardship and transfer cases. For any rapidly growing company vacancies will be a recurring problem. Scaling up typically means hiring new employees to fill lower-level positions as your more experienced team members graduate into more senior roles…although it may also require you to introduce experienced executives directly.

On a personal note, I have always been of the mindset that my most talented friends and colleagues are the critical ingredient in my success. I’ve been proud of my entrepreneurial roles as a leader and builder of company culture, head of product, head of BD, or CEO of some companies I’ve helped to found such as Palantir and Addepar. However, I’ve been lucky to have consistently replaced myself with very talented colleagues in the specific areas needed by our companies. Usually when this occurs I begin building in other areas, or my replacements choose to keep me around to help out with mentorship, strategy, or fundraising in various ways — although some of them are perfectly happy without somebody looking over their shoulder and taking credit for their work! This has helped me expand the range of projects I can channel my energy into, attract an ecosystem of brilliant, talented individuals and foster growth cultures at the companies I have been a part of.

In order for a company to grow, its team members must grow themselves — and this means personal evolution into new roles and more ambitious assignments. We admire Bloomberg’s clarity of thought, and his success as a leader suggests we should pay closer attention when he shares this kind of wisdom.

We recently put together a speech outlining the major functions of a modern Venture Capitalist. These notes from the speech articulate our basic framework for thinking about the shifting nature of the Venture Capital industry.

The Venture Capital industry currently manages about 100x what it did 30 years ago. As our industry has grown, it has evolved. The role of a modern VC has become substantially more nuanced and multifaceted than VCs of the 1970s and 1980s could have ever predicted. Today, many top Venture Capitalists are people who have started companies themselves. Venture Capitalists play a positive sum role in helping investors create value by partnering with entrepreneurs and give them every advantage possible to beat the odds and succeed. For many of us as VCs, it’s exciting to help instantiate new ideas for platforms and processes which improve how people live or how industries function. We’re eager to leverage our own experiences and networks to help entrepreneurs however we can, and continue to learn as we work on new projects.

The roles of the modern VC can be summarized as finance, community, and leadership.

As a financier, a Venture Capitalist might be:

(1) A Middleman. Wasteful Middlemen are what we like to call “New York Fabulous!” A sophisticated middleman will raise and allocate capital in a way that benefits society as a whole, rather thanfocusing on short term profits .

(2) An Expert at Structuring and Closing Deals. A VC must ensure that deals involve fair terms with no trickery as well as assigning the correct valuation to a prospective company. Deals must align the interests of parties involved so that they are mutually protected. This also applies to how a VC structures its fund vehicles.

Emerging Technology Waves

(3) Macro Analysis Investor. This is the more interesting part of finance! VCs must understand historic technology waves as well as predict emerging waves. We think that bioinformatics, smart enterprise, and transportation are three of the most important emerging technology waves as we head into 2017.

As a community builder, a Venture Capitalist might be:

(4) A savvy Network Connector for sales, customer feedback, and business development. A great VC network includes Sales, Customer Service, Business Development, and Channel Partners.

(5) A Talent Resource for hiring. VCs help portfolio companies hire top talent, and need to be able to help companies attract the right engineers, designers, sales superstars, executives, and board members.

(6) A Brand Creator for company and firm. Good brand creation is about building a trusted, respected community around your portfolio companies, which includes customer relevant networks, advisors, talent, internal operations, and your general brand. The involvement of a top VC is an important symbol for everyone around a startup — other investors, employees, potential partners and clientele. Today, the most impactful brands inside the technology world are created more with substance and success than through media. And clearly, this skill is related to a VC’s ability to build a relevant community achieve numbers four and five above for the company, as well.

As a leader, a VC might be:

(7) A Technology Consultant. In addition to providing financial support, today’s VC needs to be able to counsel portfolio companies on elements of data science, tech architecture, and design thinking. Some VCs should be fonts of advice on product or technology. Scaling a technology presents some of the hardest technical challenges for a growing company.

(8) Leadership, Management, and Strategy Mentor. Venture Capitalists serve an advisory role to budding CEOs. Top entrepreneurs are great engineers, but often not yet great leaders. Good VCs will teach entrepreneurs how to delegate authority efficiently and effectively, as well as how to scale a company. VCs who have been entrepreneurs themselves will be able to draw on their experiences to give budding CEOs specific, immediate feedback — creating value for all parties involved.

In the speech we put together — where each of these categories is a series of slides — we emphasize that not every VC plays all of these roles. Some specialize in certain areas, or have uniquely talented partners that complement each other well. But the bar has been raised and continues to climb, as investors with relevant experience and skills help startups across the board partner with leading entrepreneurs and create value. It’s amazing how this system has evolved and improved upon itself over the past decades through human ingenuity and market forces, and we are very bullish on many aspects of the top of the Silicon Valley ecosystem.

Bring in the "Adults"?

Joe|November 28, 2016

This blog addresses a recurring topic for our CEOs — how to think about the value of experience at a technology startup, the seniority of a company’s team, and when it’s the right time to make certain executive hires.

I was on the phone the other day with a talented engineer who is speaking to one of my current favorite sub-10-person companies. It was recently founded by some very talented university students, one of whom dropped out while the other finished and worked part time. These two cofounders hired their smartest friends and started building and iterating. This new potential hire was worried that the team lacks senior, experienced people and thought that it might be a bad sign.

I gave him my honest view, which is that I thought his prospect looked a lot like Palantir, FB, or many of the other great technology companies I saw early on. It has a lot of extremely talented, hard-working, and excited engineers surrounded by great advisors. My view is that they don’t need experienced people as full time employees yet. In their infancy, startups need geniuses who fit their current tight-knit culture and will iterate quickly as they push towards an ambitious vision — and they need a scaffolding of advisors, strategists, early-users and product-thinkers around these savants to guide them. Only once a company is ready to scale into a large business should it hire more seasoned, experienced management.

Those who ultimately shake up an industry are often outsiders who don’t know any better. Companies at this stage are messy and make lots of mistakes, but what matters is producing something that works and has signs of product-market fit and that learns through its early trials.

A recipe I’ve seen work in early-stage startups is a small tight-knit group of passionate people who are obsessed with their vision of how to fix a particular industry. Conversely, teams composed of people with a lot of specialized experience at running a large business are not as likely to do very well in the first year or two of a startup. Early on, what you need is rapid technical and product innovation from dangerously high IQ, often imbalanced, driven people — not a lot of high-salaried experts used to running a big machine.

You might ask: but if a startup company team is composed of a lot of inexperienced people who’ve never run a big company before, isn’t that a bad sign? Shouldn’t I join or invest in companies where there are superstars who have done it before? How can I learn if there is nobody to teach me?

The answer is that you learn primarily by building and doing — by falling on your face and getting up and falling on your face again. This isn’t to say that you don’t want great company advisors, and people around early who can help out with specialized skills or knowledge. But few mentors are going to teach you how to be an entrepreneur with vision and passion and to create something new — and that is what matters at the start.

I have seen a lot of now-great companies at their earliest stages, and these early stage startups are not built by the senior people who know how to run and scale big-company machines.

Innovation is not a business process. Of course, there may be product geniuses and serial entrepreneurs who know how to set a direction and iterate on a vision, and these types of ‘experienced’ people are helpful early on in cofounder roles. But the people who know how to run businesses processes — the company “adults” as we like to say — are often the wrong hires in year 1. These may be heads of BD or CMOs, experienced VPs of Engineering or big company HR managers to name a few. They are likely to come in and focus on things that they have learned matter… but in so doing they can obstruct innovation if the company is not ready for their skillset. I say “adults” loosely, because people well past their middle age can play the early innovative role, and an experienced executive who is brought in to help scale a company may only be in her late twenties. However, age and experience are often close proxies. Moreover it’s important to clarify that these experienced management figures are not necessarily the core leadership of a company, who will be galvanic, inspirational individuals with a broad vision of the firm’s place in the world and a well-defined set of values. Nonetheless these operational experts — “adults” — play a uniquely valuable role in scaling and streamlining a company when hired at the right time.

When is the right time to make more senior hires?

You make senior hires when you know that you need to bring in and leverage a business process — when you are instantiating something that has been repeated hundreds of times before in other contexts. At that point you can bring in somebody who knows how to optimize that process to help build that part of the organization and scale the business. Given the constantly evolving nature of a start-up it can be difficult to identify exactly when business processes are in place and an executive team should be installed; the truth is that there is no precise formula since every company and market is different. The main things to keep in mind are how to manage growing teams, keep an attention to detail and define the right KPI’s throughout your individual teams, as well as enable the CEO by reducing the number of direct reports. We’ve often seen C-suites installed after the series A, when the company is generating revenue and looking to grow based on an established view of the product and market opportunity.

Repeatable, scalable processes are where experience is key, and this is where startups often screw up. Many entrepreneurs fail to realize that as well as raw talent you should hire experienced team members as soon as you need them — the key is identifying when that is.

The mistaken thinking tends to be “We made it this far without any of these know-nothing business characters, why should we suddenly change our culture? They have nothing to teach us; business works differently than it used to, and we will figure out better processes.” Ironically, the kind of confidence that empowers you to start a company, build a great team, and achieve some early success is often a product of the same kind of over-inflated ego that will drive you to make this mistake. (I speak from personal experience in my 20's). This mentality is especially apparent in SV’s approach to MBA’s. Everyone remembers Guy Kawasaki’s tweet about valuing companies: “add $1,000,000 for every engineer, and subtract $250,000 for every MBA”, or Peter Thiel’s pronouncement that MBA’s are “high extrovert, low conviction people” a combination that he says “leads towards extremely herd-like thinking and behavior”. But the reality is more nuanced and decisions about hiring based on experience are as much a function of timing and keeping a pulse on the life-cycle of a company as any other major hiring decision. In fact, a composite analysis of “big tech companies” shows that they have more than double the proportion of job offerings requiring MBA’s than big banks and the Dow Jones Index companies. However, for many of these technology companies, the MBA’s were not around at the start — there are exceptions, but an MBA is usually tied to business scaling and negatively correlated to innovative startup leadership. Instead, they were brought in to run and iterate the business machine once their experience was needed.

If something has been done hundreds of thousands of times before, you can learn a lot by bringing in an expert. It’s hard to overestimate how valuable a great VP of sales is, and what he or she can do for your company when you need to hire sales reps, create a culture that will make smart decisions, and scale on the sales side. Or to understand why a great head of HR is so key and how this person and his or her team can complement your leadership and culture; or to realize the practices that an experienced engineering manager brings to the table and how they make your company work better as it grows… to name a few examples. Most of the first-time founders we’ve worked with who have made amazing early progress on the product and engineering side don’t actually understand what a CMO does. When they learn about what it means to map out a market and develop a strategy based on the data concerning product demand and market segment interaction they get really excited and realize they need one in order to scale. CFOs, CSOs, and many other experienced leaders also play critical roles at the right time.

The reality of a great startup is that it always feels very messy. It will always feel like you should have made key hires months ago. But startups are messy by design, especially if you are getting things right. If you ever feel like you’ve made all the hires and have all the expertise you need in-house, something is wrong and your business is going too slowly — you’ve probably way over-hired. But when you reach some sort of early product-market fit and it’s time to run businesses processes and scale, you need to make these senior hires right away — usually at least a few at once. A lot of great companies go through stages where they realize this and “upgrade” their executive team with awesome experienced talent.

In some cases I’ve seen, these hires were made late and it would have been great to have them a year earlier. In these cases, it’s tempting to wish you could have started with all of these awesome “adults” around. But in many cases bringing veteran management into the picture immediately can stultify a start-up’s culture of innovation. Some of the best Series A investments are into companies that don’t have any “adults” and aren’t quite ready for them yet. I have noticed that this stage often scares off less sophisticated technology investors from outside SV, who use the presence of these experienced experts as markers that it’s safe to invest rather than evaluating the early technology culture, metrics, and strategy. When the company is ready to bring in more senior people in order to scale, one of the roles of a great investor is to help the CEO realize this and quickly pull the trigger on the right executive hires at the right times.

“I have noticed that this stage often scares off less sophisticated technology investors from outside SV, who use the presence of these experienced experts as markers that it’s safe to invest rather than evaluating the early technology culture, metrics, and strategy.”

In conclusion, take solace in the fact that a lot of the best early-stage companies don’t have a strong “adult” presence — and focus on talent and a culture of passionate innovation instead. Don’t feel pressured to bring in experienced executives too early. But as soon as you’ve gone from 0 to 1 on the product/innovation side, you should go from 0 to 1 on hiring the experts and getting a star team of senior people around you who know how to run the machine and scale the business. Only then are you ready to say:

Our age is not short of great ideas — of ways new technology can be applied to fix global industries and increase prosperity. But we are starting to notice a serious deficit in Silicon Valley: a shortage of great leaders. A common refrain from startup entrepreneurs is that they have no problem attracting high-energy contributors, but are having difficulty finding talented, driven executives who can lead and inspire. It is growing harder to ignore SV’s leadership deficit as one of the central challenges for companies fighting to scale — and as a central question for Silicon Valley’s impact on the world at large.

Here in Silicon Valley, the term “leadership” is usually discussed with regard to effectively running and managing an organization — both of which are crucial to becoming a successful founder. But great leadership — whether in business, politics, academia or organized religion — demands more than a thin commitment to managerial efficiency. A deep concern of mine is that leaders in the technology sector have not developed a culture that insists upon courage, honor, duty and humility– what we might call a culture of virtue. The great lesson of leadership handed down to us from classical thinkers in every culture is that those who handle power must do so with a deep sense of responsibility for those whose lives they touch. One of my favorite passages on leadership comes from Sun Tzu, who writes:

Sun Tzu, Chinese General, 544–496BC

Leadership is a matter of intelligence, trustworthiness, humaneness, courage, and discipline … Reliance on intelligence alone results in rebelliousness. Exercise of humaneness alone results in weakness. Fixation on trust results in folly. Dependence on the strength of courage results in violence. Excessive discipline and sternness in command result in cruelty. When one has all five virtues together, each appropriate to its function, then one can be a leader.

Creating a billion dollar company is hard, but being a truly great leader is even harder. It requires an acrobatic balancing of commitments to stakeholders and employees with broader commitments — civic, patriotic, and global. A true leader must strive towards a grand vision of human progress, but remember that the minor details of her everyday life really matter to those who look up to her as a role model. Great leaders must understand how to act in such a way that they exhibit all the virtues in unison.

Great leaders inspire incredible loyalty in their followers and subordinates. In the 6th century, Confucius counseled, “Let him preside over them with gravity; then they will reverence him…Let him advance the good and teach the incompetent; then they will eagerly seek to be virtuous”. There are not many figures in Silicon Valley who viscerally attract followers in this way. In the tech sector it is common to find lost souls who hop from job to job, self-optimizing as quickly as possible instead of striving together towards common goals. Many would-be leaders, overwhelmed by promises they’ve made and expanding duties, go silent on allies and retrench on responsibilities. They put short-term practicalities ahead of honor and virtue. Without a conscious culture of leadership and peers to hold them responsible, executives under the increasing pressure of difficult jobs often give in to lower impulses unworthy of their own leadership potential.

Of course there are a few great leaders with legions of proud followers; there are large groups pursuing bold missions, courageously standing up to difficult challenges and making the right decisions. But these men and women are rare finds in the world of technology, and too few here are striving to understand and emulate their values. There are at least one hundred classes and meet-ups on business or tech infrastructure strategy for every one on leadership.

It’s no wonder that when entrepreneurs achieve success, they often arrogantly flaunt their newfound wealth or mistreat others with secretive or unfair liquidation preference-structures, as if their employees or former colleagues are mere instruments to securing greater personal profit. The startup mentality is intensely competitive, and fosters a spirit of “us v. them”. Taken to an extreme, this mentality can manifest itself as ruthless selfishness on the part of founders; of naked, vain ambition rather than the pursuit of a higher purpose. These kinds of viciously imbalanced worldviews reflect a culture that is crying out for stronger leaders. I’m reminded of a line by Cyrus the Great, the wisest ruler in the Persian tradition: “Success always calls for greater generosity — though most people, lost in the darkness of their own egos, treat it as an occasion for greater greed.”

Cyrus the Great, King of Persia, 600–530BC

One challenge in building leaders is what you might call the “cult of the engineer.” Our culture strongly (and correctly) emphasizes the importance of developing hard, technical mastery in computer science and related fields. No great companies here are built without a star tech culture featuring a core of elite computer scientists. Meanwhile the more intangible quality of good leadership is brushed under the rug. There is a noticeable gap between most young geniuses who excel in math and science and those who demonstrate leadership ability. It may be that the learning curve to become a sophisticated engineer is so steep that this generation’s brightest don’t have enough time to study the great leaders of antiquity, consider their place in the world from political and philosophical perspectives, or even do things as simple as playing team sports.

Building a startup that outclasses the competition may require a myopic focus on developing a sound product, but leading a company that will change the world requires just the opposite. Henri Fayol — one of the pioneers of management theory — wrote at the turn of the 19th century that “a leader who is a good administrator but technically mediocre is generally much more useful to the enterprise than if he were a brilliant technician but a mediocre administrator.” This is because leadership requires an imaginative awareness that grasps one’s environment as completely as possible, even if only imprecisely. To borrow a phrase from Isaiah Berlin, great leaders have “instinctive skill”; the power to make “inspired guesses” at the best methods to influence others and bring about their vision. George Washington, Benjamin Franklin, and Winston Churchill all possessed the power to understand the world in a broad, interdisciplinary ways — and this power to synthesize information from every quarter made them extraordinary leaders. We witness the same capacity in titans of industry and remarkable CEOs — Andrew Carnegie, John D. Rockefeller, and Steve Jobs all certainly possessed it. For an engineer gifted at coding with mechanical precision, a transition to a pure leadership role will involve a transition to a very different mode of perception — as well as a host of new interpersonal skills.

Benjamin Franklin, American Founding Father, 1706–1790AD

Silicon Valley needs to address its deficit of leadership. Initially, this will mean raising dialogue about the issue in various forums: technology summits, universities, and individual discussions. Young engineers who want to be successful on a macro-scale should understand that leadership is a skill to which they must aspire — however fuzzy a concept. For those of us in positions of leadership here in the valley, the issue demands both reflection and action. We need to help train and mentor younger leaders at the same time that we think hard about how we can best emulate history’s great leaders and heroes. What can we do to be better leaders ourselves, and to inculcate these values in our organizations and young talent? I hope this is something we can discuss more openly and more often, as Silicon Valley becomes more influential around the world.

There is an enormous literature on leadership — here are a few books we highly recommend, ranging from classics to modern leadership texts:

“Xenophon’s Cyrus the Great: The Arts of Leadership and War.” Ed. Larry Hedrick. St. Martin’s Press, 2006.

Marcus Aurelius. “Meditations.” Trans. Gregory Hays. Modern Library Edition, 2002. Print.

Sun Tzu. “The Art of War.” Trans. Lionel Giles, Chiron Academic Press, 2015.

Benjamin Franklin. “The Autobiography of Benjamin Franklin.” Dover Publishing, 1996.

Herman Hesse. “Siddhartha.” Trans. Joachim Neugroschel. Penguin Books, 1999.

Dale Carnegie. “How to Win Friends & Influence People.” Simon and Schuster, 1936.

Peter Drucker. “The Effective Executive.” Peter F. Drucker. Harper Collins, 1967.

Steven Covey. “The 7 Habits of Highly Effective People.” Free Press, 2004.

John Wooden. “Wooden on Leadership.” Ed. Steve Jamison. McGraw Hill, 2005.

Great thinkers the world over and from every time period have reflected on the concept of leadership. Here are some of our favorite quotes on the subject:

“The highest type of ruler is one of whose existence the people are barely aware.

Next comes one whom they love and praise.

Next comes one whom they fear.

Next comes one whom they despise and defy.”

-Lao-Tzu (5th-4th century BC)

“Whoever wants to become great among you must be your servant, and whoever wants to be first must be servant of all.”

-Jesus Christ, (Mark 10:43)

“The source of this predominance was not barely his power of language, but, as Thucydides assures us, the reputation of his life, and the confidence felt in his character; his manifest freedom from every kind of corruption, and superiority to all considerations of money.”

-Plutarch, writing of Pericles (1st century AD)

“There is nothing more difficult to take in hand, more perilous to conduct, or more uncertain in its success, than to take the lead in the introduction of a new order of things.”

-Niccolo Machiavelli (16th century)

“Strive to be the greatest man in your country, and you may be disappointed. Strive to be the best and you may succeed: he may well win the race that runs by himself.”

-Benjamin Franklin (18th century)

“If your actions inspire others to dream more, learn more, do more, and become more, you are a leader.”

-John Quincy Adams (18th century)

“The greatest moments in the struggle of single individuals make up a chain, in which a range of mountains of humanity are joined over thousands of years.”

-Friedrich Nietzsche (19th century)

“To be a king and wear a crown is a thing more glorious to them that see it than it is pleasant to them that bear it.”

-Queen Elizabeth (20th century)

“One’s philosophy is not best expressed in words; it is expressed in the choices one makes… and the choices we make are ultimately our responsibility.”

-Eleanor Roosevelt

“If you want to build a ship, don’t drum up the men to gather wood, divide the work, and give orders. Instead, teach them to yearn for the vast and endless sea.”

-Antoine de Saint-Exupery (20th century)

“If you just set out to be liked, you will be prepared to compromise on anything at any time, and would achieve nothing.”

-Margaret Thatcher (20th century)

“Management is doing things right; leadership is doing the right things.”

-Peter F. Drucker (20th century)

Tech Bubble or Golden Age?

Joe|July 27, 2016

There is a tide in the affairs of men

Which, taken at the flood, leads on to fortune;

Omitted, all the voyage of their life

Is bound in shallows and in miseries.

On such a full sea are we now afloat;

And we must take the current when it serves,

Or lose our ventures. — William Shakespeare, Julius Caesar.

Since the recovery from the dot-com crash, doomsday prophets have consistently warned of a bubble in the private technology company ecosystem. This may sound like a valid concern to Silicon Valley-outsiders confronted with a spectacle of far-fetched startup ideas, wild blow-ups, and the transfer of large sums of money into the hands of audacious twenty-somethings. But we are not in a tech bubble. Iterative, trial and error experimentation is the mechanism by which firms drive the evolution of the market economy; it is the natural adaptation of industry to new technological paradigms. Moreover the amount of money involved in this vital discovery process is a tiny fraction of total economic output. Like any industrial revolution, the present era is one of rapid flux of the economy in response to new technological possibilities. Economic historians looking back on the present period will characterize it as the early innings of Golden Age of the information technology revolution.

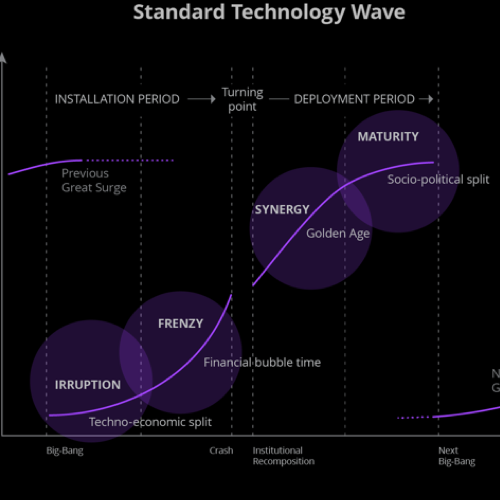

In Technological Revolutions and Financial Capital, Venezuelan economist Carlota Perez points out that our era’s first four technological revolutions all follow the same basic pattern: the eruption of the new technology, a feverish speculative frenzy, a recessionary economic collapse, a prosperous Golden Age, and a maturity phase of slowed economic growth once the technology has fully penetrated the market. Collectively, these stages result in what Schumpeter calls the “creative destruction” of the old technological paradigm. In the “installation period” leading up to the crash, the new technology disrupts and permeates friendly markets. The “deployment period” following the crash sees the dissemination of the technology into hold-out markets, rejuvenating legacy infrastructure in these industries. The standard cycle takes 50–60 years. There have been five major technological revolutions in the last 250 years: the first Industrial Revolution; the Age of Steam and Railways, the second Industrial Revolution, the automobile era, and now the Information era.

We often use Perez’s model as one guide for understanding what’s going on in the macro-economy, and what possible technological breakthroughs are on the horizon. Perez’s framework suggests that we are now in the latter half of the fifth technological revolution. The IT wave arguably began when ARPANET adopted TCP/IP in 1982, as the spine of the Information Technology revolution is the Internet. The eruption of the Internet in the 1980s phased into the dot-com bubble of the 1990s, which burst catastrophically at the dawn of the new millennium. Internet mania is an excellent example of a true bubble. Technology stocks soared 300% from 1997 to 2000, and accounted for 35% of total public investment at the peak. P/E ratios were at astronomical levels, and paper fortunes were rapidly being made. But many stocks had zero profits and valuations were disconnected from discounted future cash flows. The crash was the turning point for the IT revolution.

If the crash of 2000 represented the turning point, then 2016 is the Golden Age of the information technology wave. Each wave lasts for around 50–60 years, and we are now in the middle of the deployment period. In the deployment period, the current technological paradigm will fully commercialize. Technology producers will control an increasingly large share of resources as they work to transform old business infrastructures and improve the lives of consumers. We are transitioning from the speculative, “casino economy” of the 1990s to a period where financial capital reconnects with builders and doers — those who scale functional platforms to create real value in an economy. As we move into the deployment phase of this IT wave, angel investing will become less profitable than growth-stage investing, as the real opportunity for capturing value creation will occur as young but growing enterprise companies expand to their full potential. Venture capital will continue to consolidate into those few larger firms poised to aggressively scale their novel, industry-winning data and workflow platforms.

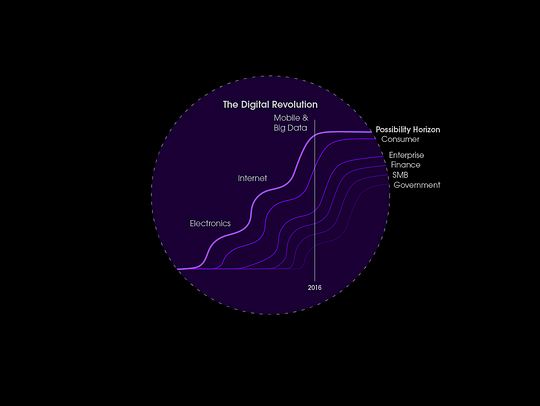

The unique thing about the current technological revolution is that a series of new innovations have “lifted” or “bumped” the possibility curve upwards and exaggerated the shape of the normal technology wave. If the Internet were a standard technology curve, then a post-2000 world would see the deployment of similar kinds of companies that existed pre-2000, perhaps with small iterations. But something different has happened. In the last 16 years, there have been several other inventions that have compounded the growth of the Internet era and pushed the bounds of what is possible. The invention and commercialization of the smartphone is one such example. In 2000, before the iPhone came to market, there were only 50 million people on the web. Today, there are 3 billion people online, with the majority of traffic driven by mobile.

Perhaps most importantly, the technology underlying the IT paradigm continues to rapidly increase in capacity. Since the dot-com crash of the early 2000s, the continual miniaturization of transistors and the compounding exponential growth of computational power has progressed so far that it has massively distorted the shape of the curve. Companies can now host their data on cloud providers such as Amazon on Microsoft, where they can spin up or down their storage as necessary. Paired with the commoditization of big data analytics frameworks such as Hadoop, this shift has opened the door for organizations to process and analyze hundreds of millions of data points in seconds. Companies can now solve complex, non-linear problems in ways that were not possible with the software built at the beginning of the IT wave in the 1970s and ’80s. The consequence of this extension of the installation period of the IT Revolution is what we have elsewhere been calling the “Smart Enterprise” wave.

Borrowing Perez’s terminology, each of these minor technological developments generates a kind of miniature installation period and market craze of its own. Successive inventions are creating new applications for the Internet as new devices and software connect to the cloud. In the present Golden Age, installation and deployment dynamics operate in tandem. Collectively, this process is fueling new opportunities to capitalize on the IT wave. Some of our partners and friends disagree with us on the question of whether new paradigm shifts will take place in the next decade. For instance, futurist Ray Kurzweil suggests that the rate of innovation is itself accelerating, and that new paradigms will occur at ever closer intervals in the future. Our view, however, is that the Smart Enterprise paradigm will remain the dominant one for the full generation predicted by Perez’s model, and that no upcoming paradigm (e.g. virtual reality, artificial intelligence) will be as transformative to the overall economy for quite some time. If our view is correct, then the best opportunities for putting capital to work will be at the growth stages of Smart Enterprise companies. That is not to say that there won’t be good opportunity for angels to capture in the Installation Phase of the next paradigm, or at the tail end of the Smart Enterprise wave. But the best opportunities will more and more skew towards Smart Enterprise companies with signs of early success and with 99% of the market left to capture. Consistent with this view, we are launching a co-invest fund to fuel companies poised to aggressively scale their platforms.

A technological revolution is like a rock thrown into a placid pond. It takes time for the ripples to reach the pond’s edge. As Perez notes, techno-economic paradigms “are highly uneven in coverage and timing, by sectors and by regions, in each country and across the world.” The Internet/big-data splash rippled through the consumer space in the 1990s and early 2000s, generating companies like Google, Facebook, and Amazon (the “Consumer Wave”), and creating enormous value. As depicted in the graphic below, it is now impacting a variety of formerly sequestered industries such as energy, finance, and government. These are trillion dollar industries with archaic information systems, employing human beings as middleware to perform routine data-processing and communication tasks. Perez explains that “institutional recomposition” occurs in the deployment period. Indeed, in our era, inefficient back-end infrastructure is being updated with state of the art information gathering, structuring, and analytics techniques– i.e. “Smart Enterprise” software.

The next generation of Smart Enterprise companies will create network effects by concentrating anonymized data from across the entire industry such that the more users there are, the better the industry data will become. Storage and cloud-computing will continue to become cheaper, more data will be created and processed, and progress in deep learning, neural nets, and AI will oust more and more human middleware. The Smart Enterprise wave will thus free up human minds for tackling questions which demand high levels of abstraction and creativity. Still, though, there will need to be a layer of human decision-making in core business processes for the foreseeable future.

In the excitement of Silicon Valley speculation, it’s important not to lose sight of the grander narrative of technological progress. The vast majority of the economy has yet to be transformed by the IT revolution — we are nowhere near the exhausted, fully-saturated markets of Perez’s “maturity” phase.Unlike the early consumer platforms, which have now attained behemoth status, the first flight of Smart Enterprise platforms have only touched a fraction of the major parts of the economy they are destined to impact. It is likely that Silicon Valley has already developed many if not the majority of the breakthroughs relevant to the current technological generation, and that Smart Enterprise companies are beginning to transition from adolescence to early adulthood. Over the coming decade, the most compelling opportunities will increasingly be these scaling-phase platform ventures, which will raise large amounts of capital and grow at high rates for years longer than most expect — generating exceptional financial returns. While the current zero interest-rate macroeconomic environment suggests that we may be in a macro-economic bubble, the technology sector is not a culprit. Perez’s model helps demonstrate that we are instead in the most productive period of the IT revolution, or in the words of the Bard, “afloat on the full sea of fortune.”

Joe Lonsdale

Partner, 8VC

Founder, Palantir and Addepar

Reid Spitz

Investor, 8VC

Clay Spence

Writer, 8VC

Mentorship and Problem Solving with Secretary George Shultz

Joe|July 7, 2016

Secretary George Shultz, born 1920, great American economist, statesman, and businessman.

Secretary Shultz is one of the great men of our age, and I am lucky to have gotten to know him over the past several years during his time at the Hoover Institute at Stanford. Born in 1920, he has lived an extraordinary life and is still actively working on some of the most important problems of our time including nuclear non-proliferation and mentorship of government leaders.

Shultz hardly needs an introduction — an economist, statesman, and businessman, he has served in four Presidential administrations in a variety of roles including Secretary of Labor, Director of the OMB, Secretary of Treasury, and Secretary of State. He is an extraordinary polymath; a man admired by many leaders from all backgrounds.

Zac Bookman — my co-founder of OpenGov and the company’s CEO — and I visited him at his office recently to show off the progress at OpenGov and to get his advice in other areas. The Secretary is an advisor to OpenGov and we are excited to hear he plans to visit our team again soon. We were proud to show him that we have deployed the technology to over 1000 cities and districts, from 0 when we first discussed the idea with him, and to see his excitement about programs we are rolling out to make government work better. Although OpenGov was one topic, I was so inspired by other parts of our conversation and by the Secretary’s stories that I thought it would be fitting on America’s Independence Day this year to share some of this great American’s wisdom.

When Ideologies Clash, Focus on Problem Solving vs. Principals

In the early seventies, President Nixon put Vice President Spiro Agnew and Secretary Shultz in charge of getting rid of school segregation in the seven states that resisted earlier court rulings. Agnew didn’t want to touch the topic because he saw it as politically destructive, so Secretary Shultz jumped in and started working on the problem. Emotions were high and confronting this sensitive issue was tough going at first, but Shultz persevered and set up multi-racial commissions of leaders in each of the seven states. When he met with the commissions, he’d steer them away from ideological conversations and instead talk about the problems that needed to be solved — he would have them agree on the problems and discuss possible solutions.

“People are great problem solvers — it’s what we do,” he told us. By applying his leadership and persuasion and getting people to agree on a problem and work together to solve it, versus arguing about principles, groups overcame their differences and successfully eliminated segregation in many of the most stubborn parts of the southern US.

Make It Their Idea, and Work Behind the Scenes

It almost seems like a fantasy in this day and age, but when Secretary Shultz came up with a tax reform idea under President Reagan, he was able to get it passed 97 to 3 in the US Senate.

The reform lowered the tax rate in the top tax brackets for corporations but was revenue-neutral as it eliminated a lot of loopholes. Rather than take credit for the idea, which he knew would lead to opposition by the Secretary of Treasury and others in the White House, he convinced President Reagan to make it his idea. Then he worked behind the scenes with leaders on the left, found what was important to them, and got them to propose something similar. By having dialogue with both sides and empowering each to push forward what they wanted, his leadership and the trust he had from all sides enabled him to guide the reform through with nearly unanimous support.

Secretary Shultz never got credit for much of what he did, but he did earn great respect from many people on the inside. This is what true leadership looks like, and we can’t help but wish we had more men like him in government today.

Not Bi-Partisan, Mr. President — Non-Partisan

When Shultz and Henry Kissinger were visiting President Obama at the White House to discuss nuclear non-proliferation, the President commented that it was great to see much needed bi-partisan work being done. The Secretary corrected the President; the work wasn’t bi-partisan, it was non-partisan. Partisanship had nothing to do with it — some issues are just about what’s best for America and the world, regardless of parties. Rather than always see the world through the lens of parties and the goals of both sides, which leads to a constant “us-vs.-them” mentality, it’s good to carve out as much as you can and work together to achieve common goals.

The perspective of non-partisan goals and accomplishments is a refreshing paradigm; one that is emblematic of an older style of American leadership that would be very welcome in today’s hyper-polarized political environment.

The Shultz Rule

Another great American, our friend and investor Sam Reeves, took my 8VC partner Drew and my father and I golfing at his club at Cypress Point for father’s day this year. Many of the members knew and admired Secretary Shultz, so the golf course came up when I saw him the next week.

The Shultz Rule on hole 16 at Cypress Point speaks to the Secretary’s personality.

He asked how I did on hole 16, which is either played as an easy par 4, or else a particularly challenging 230-yard par 3 over a beautiful stretch of California ocean and cliffs. I went for it twice in a row, and the first ball bounced off the cliffs 220 yards away, but the second one ended up on the green. The Shultz Rule, created amongst his friends, says that if you take the risky and daring shot and go for the green, you get a mulligan (one free do-over) if you miss. By his logic, I was on in 1! His rule encapsulated a few things about the great man — both his bold nature and playful spirit… as well as his sense of diplomacy. It’s worth trying for greatness — and it’s worth having fun!

We are really lucky to have a man like Secretary George Shultz in our lives, and his lessons are particularly apt for today’s leaders.

Benjamin Franklin, American Founding Father, 1706–1790AD

Benjamin Franklin, American Founding Father, 1706–1790AD